You can still get money to help you cope with the increasing costs of payroll. You do NOT need to be in the hardest-hit sectors or in the tourism and hospitality industry to be eligible for this wage subsidy.

The program ends on May 7, 2022, but it is retroactive, and applications are accepted up to 180 after the end of a period (Nov. 3 is the last day you can apply for the last period). So, the sooner you apply, the more money you can get!

How does CRHP work?

- Revenue loss needed: at least 10%

- Wages eligible:

- New hires

- Increased hours or wages of existing employees

- Retroactive applications: you can apply up to 180 days after the end of a claim period.

- Subsidy available: Up to 50% of the remuneration that exceeds the remuneration you paid during the reference period (March 14, 2021, to April 10, 2021).

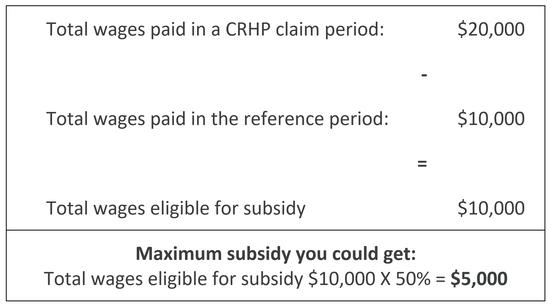

Example:

In the example above, you could get up to $5,000. Your business could surely make good use of this kind of money!

| Periods | Period dates | Last day to claim CRHP |

|---|---|---|

| Period 22 | Oct 24 to Nov 20, 2021 | May 19, 2022 |

| Period 23 | Nov 21 to Dec 18, 2021 | June 16, 2022 |

| Period 24 | Dec 19, 2021, to Jan 15, 2022 | July 14, 2022 |

| Period 25 | Jan 16 to Feb 12, 2022 | August 11, 2022 |

| Period 26 | Feb 13 to Mar 12, 2022 | September 8, 2022 |

| Period 27 | Mar 13 to Apr 9, 2022 | October 6, 2022 |

| Period 28 | Apr 10 to May 7, 2022 | November 3, 2022 |

Don’t wait! See below for all the details to know if you qualify or talk to our advisors at 1-833-568-2342 if you need help or have questions.

What is the CRHP?

The Canada Recovery Hiring Program (CRHP) is a hiring subsidy which will support employers with a subsidy of up to 50% on incremental remuneration paid to eligible working employees (I.e., the portion of remuneration exceeding the remuneration of the baseline period). It will be offered until May 7, 2022, to qualifying employers who have seen a drop in revenue due to COVID-19. During the periods where applicants are eligible for the CEWS, they will have the choice of benefiting from either the CRHP or the CEWS with a declining rate.

Most recent update:

On December 17, 2021, Bill C-2 received Royal Assent, extending the Canada Recovery Hiring Program until May 7, 2022.

As more details are available, we’ll update our website with the most accurate, recent information.

Visit our COVID-19 Help Centre

Our primary concern at CFIB is making sure you have the support you need to get through this uncertain and challenging time. We provide you with expert advice and ensure that you have all of the latest information on government announcements and available support.