The US has been able to surcharge credit card transactions since January 27, 2013

.png)

A recent survey of CFIB members found that 19% of merchants are considering surcharging customers when they pay by credit card

%201.png)

One-in-two businesses report credit card fees have increased in-store in the last 3 years

How to Claim

Starting May 30, 2022, you can submit a claim through the Credit Card Class Action website. What you will need to know:

• Name

• Contact information

• Size of your business / annual revenues during the claim period (can be classified as a small, medium, or large business – see table below)

• Attestation that you collected credit card payments at some point since March 23, 2001 – more information to come on details of attestation requirements

Note: No documentation is required for merchants classified as “small businesses”.

Process

You will receive confirmation that your claim was submitted successfully. Your application will then be reviewed and either approved or denied.

If you are approved, you can expect to receive your funds before the end of 2022 by direct deposit or cheque (opting for a cheque will deduct $2 from your claim).

If you are denied, you will receive a decision notice. No appeal process exists for small business claims. If you have any concerns, you can speak to the claim administrator.

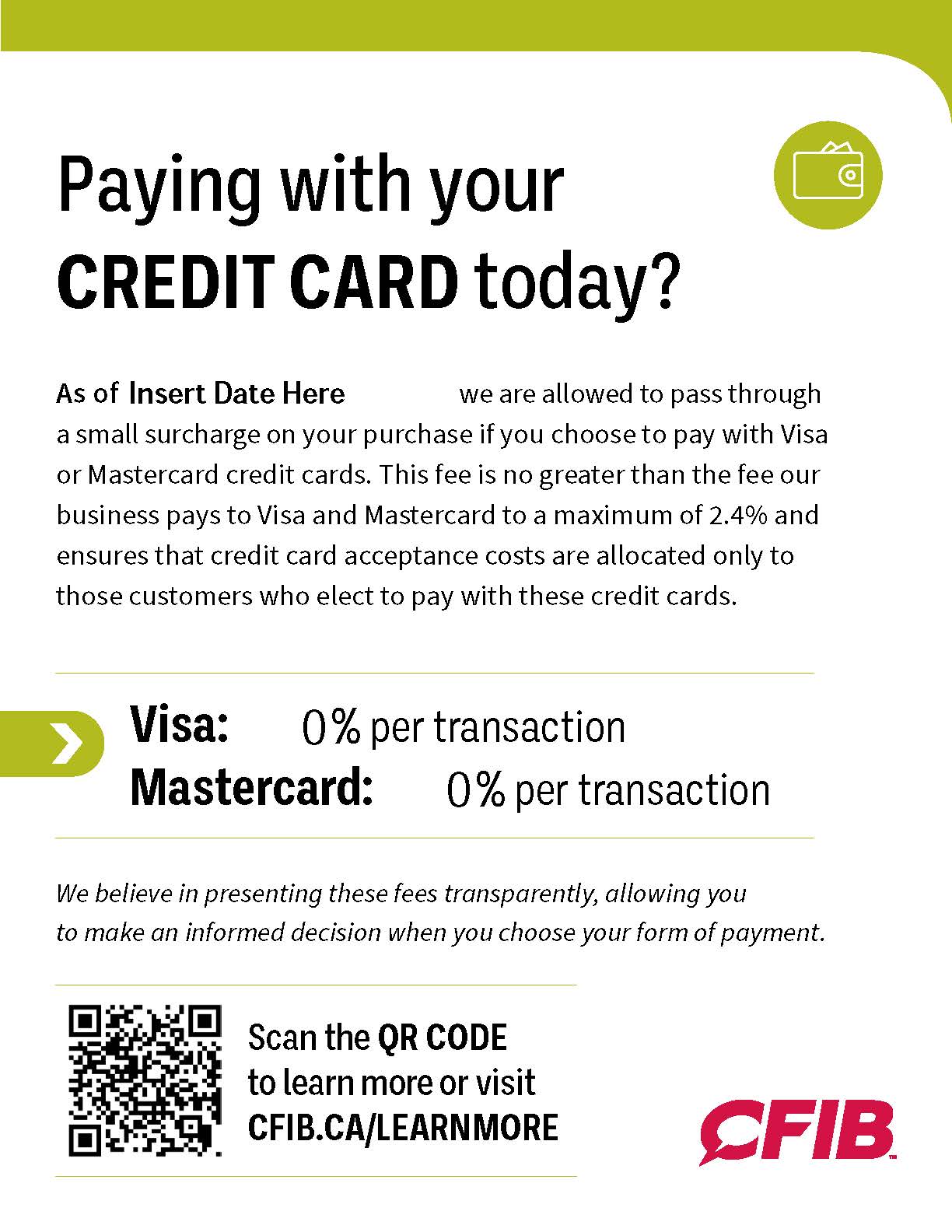

Why surcharging matters

Credit card processing fees can be very difficult to track and come with a significant cost. Over the years, merchants have seen these costs rise, especially smaller merchants who often pay much more than larger companies to accept credit cards making it more difficult for them to compete with large companies. Businesses should be allowed to explain to their customers why their prices increase and decide if they will pass this cost to their customers.

Until now, most businesses were not permitted to surcharge. Following a class action lawsuit, Visa and Mastercard are allowing businesses to pass along the cost of processing a credit card transaction to consumers.

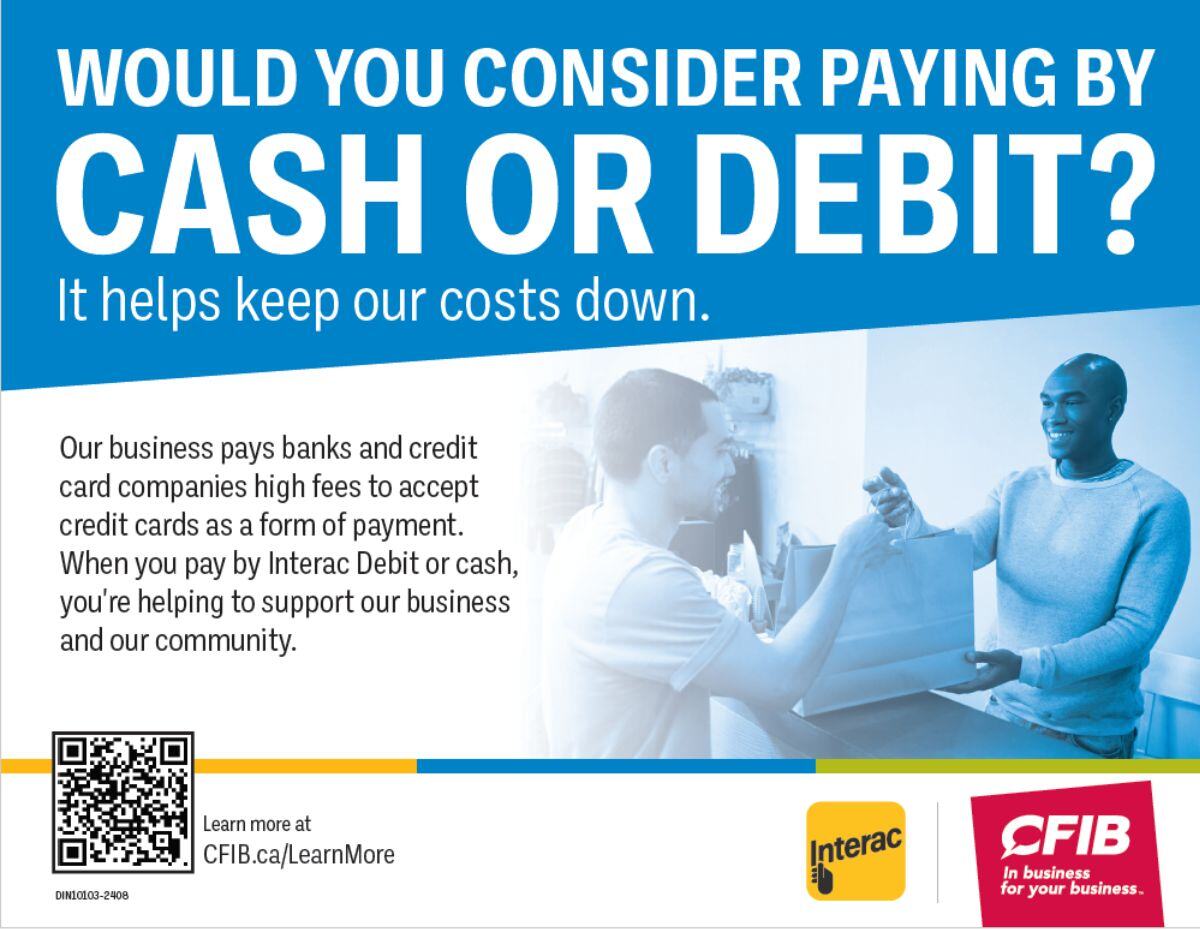

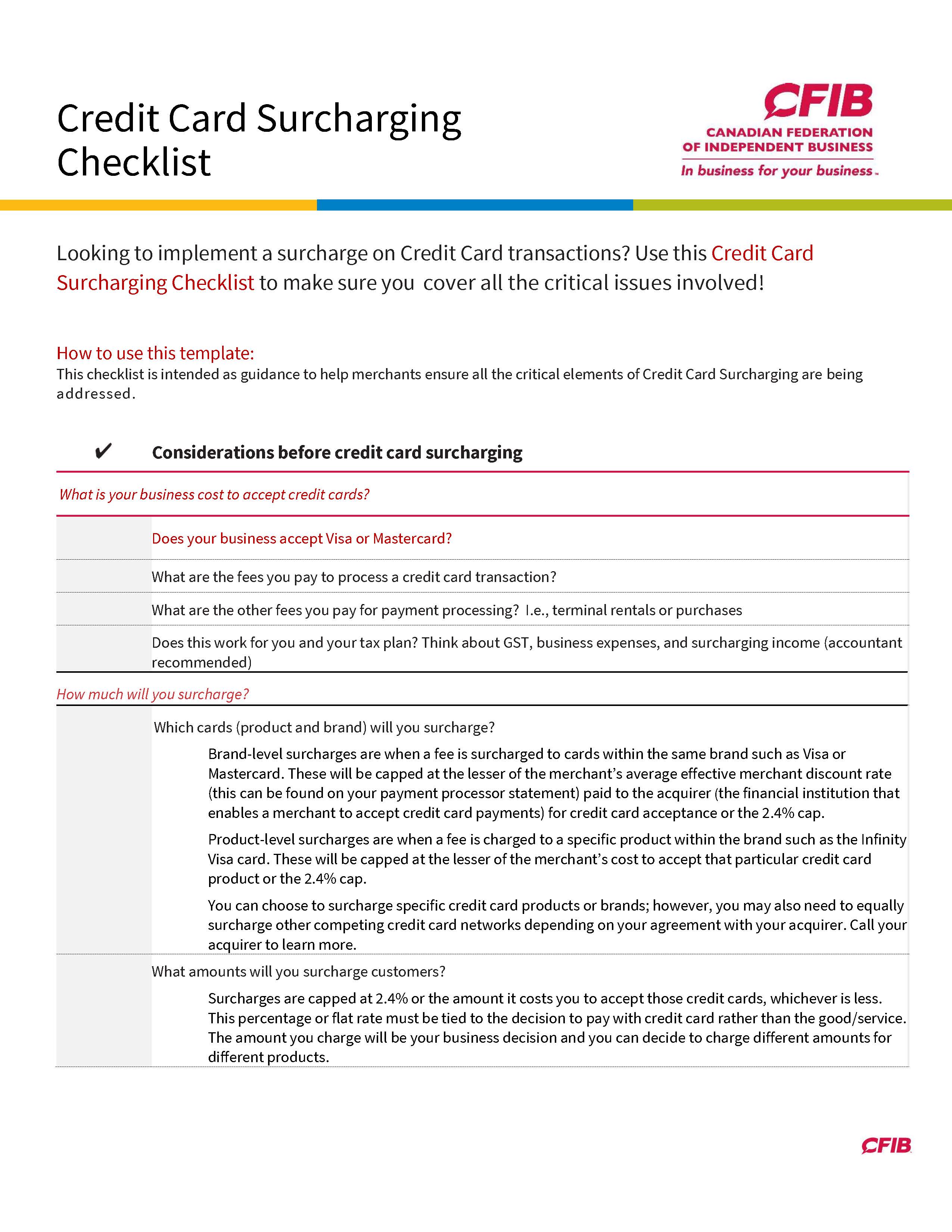

Printable Posters & Templates

Whether you are looking to surcharge or encourage consumers to use alternatives like debit or cash, CFIB has posters, checklists, and email templates to suit your business needs.

Templates

.png?width=690&height=690&name=MicrosoftTeams-image%20(26).png)

With your support, we will continue to fight for:

- Lower interchange fees

- No swipe fees on GST/HST

- More fairness for merchants on “chargebacks”

- No fees on prepaid cards and refunds

Save even more on your credit and debit processing costs with CFIB

Looking for fair contracts and even more savings? CFIB members have access to exclusive low rates with Chase, one of Canada’s leading payment processors. Learn more here or speak to one of our Business Advisors at 1-833-568-2342 to ask any questions about the class action.