Hidden secret to retiring early in the public sector

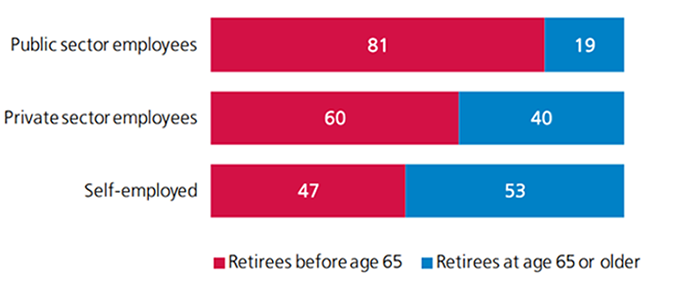

Most public sector employees enjoy retirement savings plans that are more generous than those available to their counterparts in the private sector. As such, it’s not surprising that public sector workers would receive far more in their retirement than their counterparts in the private sector, or that a higher proportion leave the workforce before age 65 (See Figure 1). Not as apparent, however, are the incentives public sector workers receive to retire early (before age 65)—namely the bridge benefit.

Figure 1: Retirees before age 65 vs. retirees at age 65 or older, by sector, average for 2007-2011 (% Retirees)1

With the Canada/Quebec Pension Plan (CPP/QPP) the standard age for collecting benefits is age 65, however, benefits could be collected as early as age 60. Those who elect to receive their CPP/QPP benefits before age 65 are penalized with lower payments than they would receive if they had waited until they were 65.

For many private sector workers, the penalty for collecting CPP/QPP benefits before age 65 may deter them from retiring early—not so for many public sector workers.

In addition to their annual pension, many public sector pension plans offer an additional temporary benefit (bridge benefit) to workers who retire prior to age 65. In most cases, the bridge benefit amount is more or less equal to the unreduced CPP/QPP benefit that they would otherwise be eligible to receive at age 65, and it is designed to continue until they reach 65 years of age. Further, most public sector pension plans also allow early pensioners (between ages 60-64) the option to begin receiving a reduced CPP/QPP pension along with the bridge benefit.

In effect, unlike their counterparts in the private sector, not only can public sector workers receive a benefit equivalent to their unreduced CPP/QPP benefits prior to 65, they also effectively receive it as compensation for retiring early.

The federal and most provincial public sector pension plans—with the exception of Alberta, Saskatchewan, and Manitoba—offer a bridge benefit (see Table 1).

| Province | Name of Plan | Annual Bridge Benefit Amount |

| British Columbia | Public Service Pension Plan | $8,190 |

| Alberta | Public Service Pension Plan | N/A |

| Saskatchewan | The Public Employees Pension Plan | N/A |

| Manitoba | Civil Service Superannuation Plan | N/A |

| Ontario | Public Service Pension Plan | $8,607 |

| Quebec | Government and Public Employees Retirement Plan | $8,373 |

| New Brunswick | Public Service Shared Risk Plan | $8,327 |

| Prince Edward Island | The Civil Service Superannuation Fund | $8,820 |

| Nova Scotia | Public Service Superannuation Plan | $8,373 |

| Newfoundland and Labrador | Public Service Pension Plan | $7,378 |

| Federal | Public Service Pension Plan | $7,476 |

Note: This table is an example of the Bridge Benefit amount for a public sector worker retiring in 2014 at age 60 with 24 years of pensionable service and an average salary of $60,000.

Members of provincial and federal plans are eligible to retire as early as 55. In terms of the bridge benefit, providing public sector workers the ability to collect the benefit at such early ages can be costly to both provincial and federal public sector pension plans. For example, the total cost to the federal plan associated with delivering the bridge benefit to over 55,000 early retirees in 2010-2011 was approximately $385 million, given that the average bridge benefit received was approximately $7,000. Such costs can be expected to increase as baby-boomers begin to retire in large numbers.

Providing government workers with a bridge benefit is a costly and unfair practice; that simply does not exist in the private sector. Indeed, in the past, entities such as the Bank of Canada found that this practice was unsustainable and thus the Bank decided to eliminate it from its pension plan2.

Recommendation

- To bring fairness and sustainability back into the public sector pension system, CFIB is asking that governments (federal and provincial) eliminate the bridge benefit.

[1] This Research Snapshot is based on the full report The Case for Ending Early Retirement in the Public Sector. CFIB. 2013.

[2] The Bank of Canada Pension Plan (By-law 15) was amended, effective January 1, 2012, to (among other things) remove the bridge pension benefit. This change applies to members of the Plan whose employment by the Bank commences on or after January 1, 2012.

Share Article

Share Article

Print Article

Print Article