Summary

- The Small Business Deduction (SBD) is widely misunderstood. Far from discouraging growth or misallocating capital, it helps many small firms overcome structural constraints—whether they are growing or simply right‑sized.

- In the near term, the SBD should be strengthened. Restoring its value and simplifying its design would help Canadian entrepreneurs stay competitive, reinvest, and grow our economy.

- Over the longer run, Canada should modernize how it taxes business income. Reducing reliance on suboptimal corporate taxation—potentially through a distribution‑based system—would make the tax system more efficient while continuing to address many of the flaws the SBD is asked to compensate for today.

Introduction

Taxes have consistently ranked among the top concerns for Canadian business owners for decades. CFIB data show that the total tax burden has been the most frequently cited issue for entrepreneurs for at least 25 years—well ahead of other major challenges such as labour shortages or red tape. What has changed is not the nature of the concern, but some of the context in which it is felt.

Today’s conditions help explain why tax pressures remain a top worry for entrepreneurs. Small businesses today face historically high operating costs, elevated borrowing rates, regulatory complexity, and ongoing economic uncertainty. In this environment, tax relief that improves cash flow and supports reinvestment is not a luxury; it is a stabilizing force.

CFIB surveys consistently show strong support for cutting the small business corporate income tax, a lower tax rate effectively delivered through the Small Business Deduction (SBD). For many entrepreneurs, the SBD, far from being a niche benefit, is a core support for running and growing their business. It directly improves their ability to pay staff, invest in their operations, and ride out economic shocks

Figure 1: Tax cuts most favoured by small business owners

Source: CFIB, Your Voice survey, July 10-24, 2025, n = 2,044.

Question: If governments (federal, provincial/territorial and municipal) were to reduce taxes, which areas should be prioritized for tax cuts? (Select all that apply)

*Note: ‘Provincial payroll taxes’ was only asked in provinces collecting it (NL, QC, ON, MB, BC).

Yet the SBD is also one of the most debated elements of Canada’s tax system. Critics argue it discourages growth, misallocates investment, and benefits the wrong people. The following takes a closer look at those claims and asks a simple question: what does the evidence actually show—and what should policy do next?

What the SBD is—and why it exists

The Small Business Deduction lowers the tax rate on the first portion of active business income earned by Canadian‑controlled private corporations (CCPCs), which make up most Canadian SMEs. The underlying policy logic is straightforward: small businesses face higher costs, fewer financing options, and less room to absorb risk than larger firms. A lower tax rate helps offset these disadvantages and supports reinvestment.

Preferential tax treatment for small businesses is not a recent invention. Canada has maintained lower tax rates on the first dollars of business income in some form since 1949. Today, roughly half of OECD countries provide explicit small‑business tax relief through reduced rates, graduated systems, exemptions, or other mechanisms.

Uniquely in Canada, the system delivers the lower rate through a deduction rather than a lower statutory rate, which was the result of a compromise reached after the federal tax reform of 1972. The federal SBD was originally set to limit access to a lower 25% corporate tax rate to the first $50,000 of active business income of CCPCs.

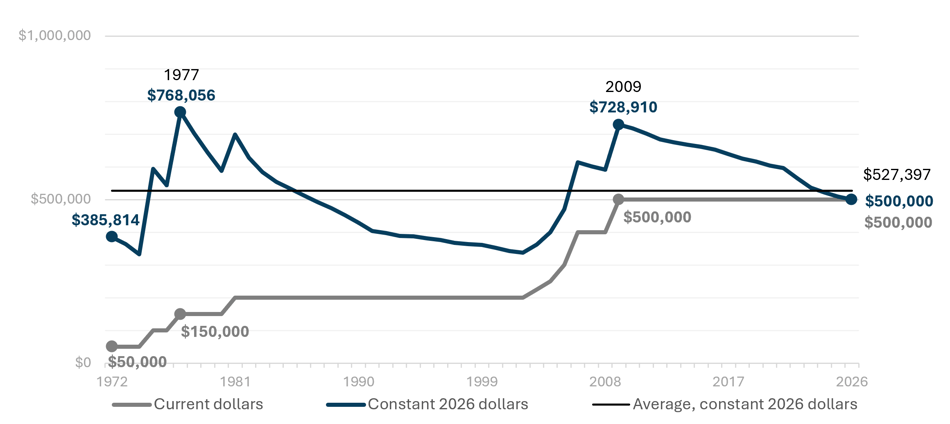

The limit has since been raised multiple times, with its value in constant dollars averaging more than $527,000 between 1972 and 2026, as shown below.

Figure 2: Canada: Federal Small Business Deduction income limit, 1972-2026

Calculations and Source: CFIB and Finances of the Nation.

Two key insights emerge from this figure:

- Repeated attempts—most notably in 1977 and 2009—to push the limit to the 2026 equivalent of a $700,000–$800,000 range; and,

- A highly irregular adjustment pattern where any increase has been quickly wiped out by inflation in the following years, underscoring the absence of an indexation mechanism.

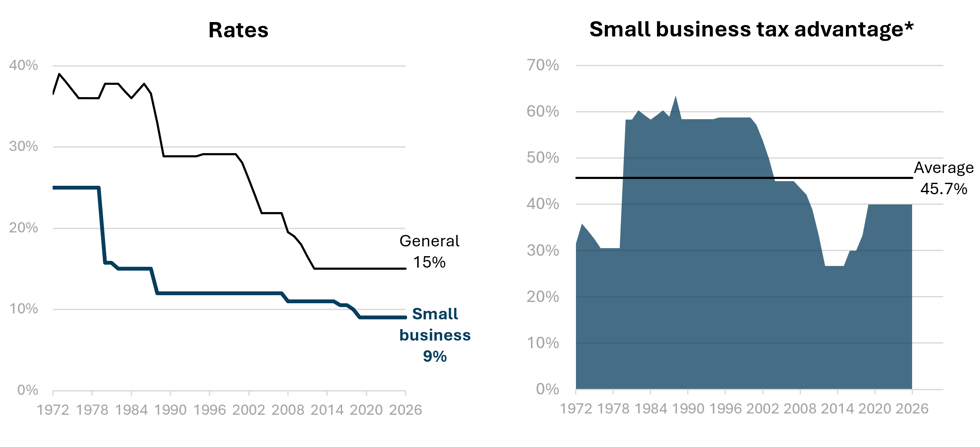

Although the real value of the SBD limit has fluctuated over time, the small‑business tax rate itself has steadily declined, from 25% in 1972 to 9% in 2026. Over the same period, the general corporate rate for large firms fell even faster, from 36.5% to 15%. This convergence has narrowed the small‑business tax advantage, which ranges from 0% when the two rates are equal, to 100% when small‑business income is tax‑free. The result is a paradox: despite historically low rates, the small‑business advantage (about 40% in 2026) is weaker than in the past and now sits below its historical average of 45.7%.

Figure 3: Federal corporate tax rates, Canada, 1972-2026

Sources: Calculations and source: CFIB and Finances of the Nation. * The small business tax advantage is the difference between the general and

small business rates, expressed as a proportion of the general rate.

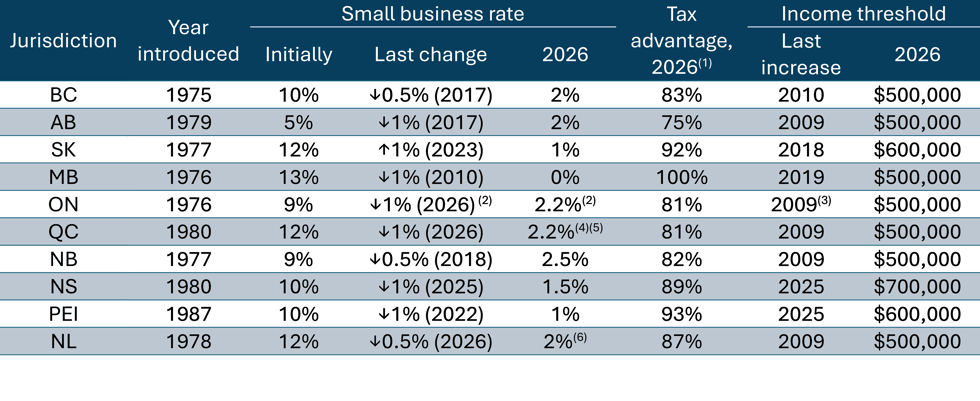

After the 1972 federal tax reform, provinces gradually adopted their own small business deductions and then progressively reduced their rates to maintain the tax advantage offered to small businesses, as seen in the table below.

Figure 4: Small Business Deduction, key features for provinces

Sources: Source and calculations: CFIB, Finances of the Nation, Canada Revenue Agency, EY, BDO.

(1) The small business tax advantage, which can range from 0% when the two rates are equal to 100% when small‑business income is tax‑free, is the difference between the general and small business rates, expressed as a proportion of the general rate.

(2) The 2026 Ontario budget is proposing to cut the small business tax rate from 3.2% to 2.2%, effective July 1, 2026.

(3) Year announced, with a retroactive start to 2007.

(4) New rate announced as effective immediately on April 29, 2026.

(5) For small construction and services businesses with less than 5,000 hours worked by all staff annually, Quebec applies the general corporate rate of 11.5% (the lower SBD rate is phased-in linearly between 5,000 and 5,500 hours). The stated intention behind this counter-intuitive measure is to incentivize the smallest firms to grow.

(6) April 29, 2026 budget announcement: rate reduced to 2% as of January 1, 2026 (retroactive); 1.5 % on January 1, 2027; and 1 % on January 1, 2028.

This table shows that provinces have leapfrogged Ottawa in adopting a more small‑business‑friendly approach to the SBD, through:

- Post‑pandemic rate cuts (while the last federal cut was in 2019);

- Much lower small‑business rates in 2026, averaging 1.6% across provinces versus 9% federally;

- A stronger tax advantage in 2026, averaging 86% provincially compared with 40% federally; and,

- Higher SBD income thresholds in Saskatchewan, Nova Scotia, and PEI.

Taking a closer look at common SBD claims

Much of the criticism directed at the SBD rests on strong theoretical claims and weak real-world support. When we look at how small businesses actually behave, those concerns largely fade.

Claim: The SBD discourages business growth

Perhaps the most common criticism of the SBD is that it creates a disincentive to grow. Because the lower rate applies only up to a fixed income threshold, critics argue that firms will deliberately cap their growth to remain eligible.

At the core of this argument is an implausible assumption: that rational entrepreneurs would willingly forgo meaningful additional revenue simply to avoid paying a fraction of it in taxes.

In any case, it would be a serious concern if this behaviour were widespread, but the data show it is definitely not.

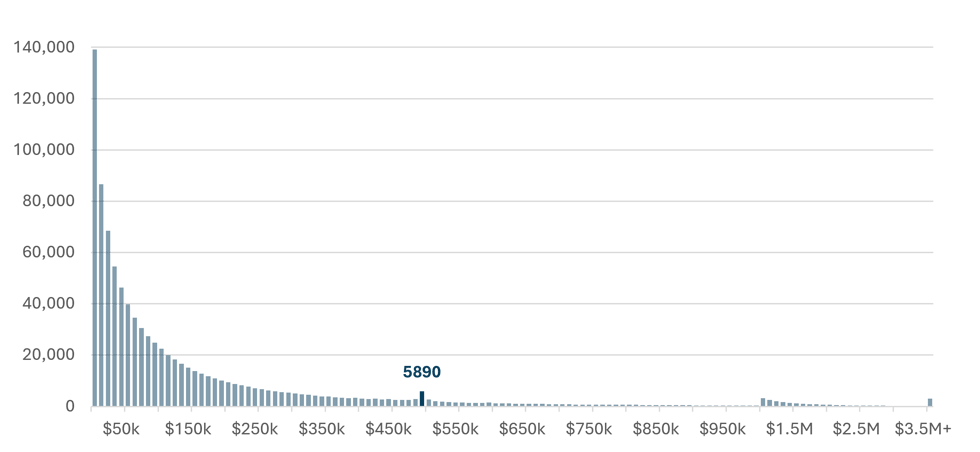

An updated version of earlier CFIB research published in the Canadian Tax Journal, this time based on 2024 federal tax data on 911,920 SBD claimants that year, paint a clear picture:

- 43% of claimants reported less than $50,000 in taxable income;

- 77% reported less than $200,000; and,

- 89% reported less than $400,000.

In other words, the vast majority of firms claiming the SBD operate far below the threshold.

Second, only a very small number of firms (5,890) bunch just below the current $500,000 limit. After adjusting for what would be there anyway under a smooth income distribution, the results suggest that about 3,900 businesses—or 0.4% of SBD claimants—may be constraining income to remain eligible. That means at least 99.6% of SBD claimants are not limiting their growth because of the deduction.

Figure 5: Small business deduction claimants, by taxable income category, Canada, 2024

Source: CFIB and Canada Revenue Agency

Third, and importantly, research also shows that “bunching” is often temporary and driven by real business decisions. A 2025 Statistics Canada study finds that firms near the threshold tend to bring forward capital purchases—such as equipment or vehicles—to reduce taxable income. This behaviour reflects accelerated investment, the actual opposite of suppressed growth. The study also shows that vehicle and machinery‑and‑equipment purchases are the main tools used for firms near the threshold, and that a majority of those users are one‑time bunchers (54%), with the remainder engaging more strategically. This indicates that counter-productive or sustained income suppression to avoid the threshold is likely a minority approach even among bunchers.

The data point to a clear conclusion: any notion that the SBD is a meaningful barrier to growth is overstated. For virtually all firms, as we will see later, the constraints on expansion have far more to do with financing, labour, regulation, and market conditions than with tax thresholds.

Claim: the SBD does not efficiently target firms that want to grow

One common claim is that the SBD fails to efficiently target firms that want to grow. Critics often point to the federal government’s stated rationale for the SBD—helping small firms overcome higher financing costs and generate after‑tax income for reinvestment—and argue that firms without growth plans fall outside that purpose.

This view is too narrow. Not all productive or successful SMEs are built to grow rapidly, and many deliberately remain small or mid‑sized for good reasons. As we outlined in a previous blog, in the real world frictions and rational fit indeed often keep firms small or mid-sized, with labour constraints, owner capacity, market access and size, risk tolerance, and operational fit all being notable influences, among others.

Moreover, financial institutions have very limited ways of determining which businesses are going to grow and which ones aren't. Even if allocating the tax preference to growing firms was fair and a good idea, it would be impossible to do with any degree of accuracy. Firms in any sector may grow or not.

Public policy should reflect this reality. Growth is valuable where it makes sense, but it is not the only measure of success. Small and medium-sized firms face structural disadvantages simply by being small, including higher per-employee regulatory costs, limited access to tax planning, barriers to government programs, and exclusion from public procurement. These challenges affect firms regardless of whether they plan to scale.

The SBD responds to these realities. It supports viability, resilience, and reinvestment across the SME sector, not just among firms pursuing rapid expansion. Limiting the SBD only to “high‑growth” firms would miss much of the problems it should address.

Claim: The SBD misallocates capital toward small firms

Another critique is that the SBD distorts capital allocation by favouring small businesses over larger, potentially more productive firms. In a textbook model, capital should flow to its highest‑return use, and tax preferences interfere with that process.

This argument assumes capital markets work equally well for all firms. In reality, they do not.

Small businesses face well‑documented financing barriers, including higher borrowing costs, more stringent conditions, and information gaps with lenders. CFIB research consistently shows that smaller firms are less likely to have loan applications approved and, when approved, face higher interest rates and are more likely to be required to pledge personal collateral.

In this environment, many viable small‑business investments are underfunded, even when they generate strong economic and social returns. The SBD helps bridge that gap by allowing firms to retain more after‑tax earnings and rely less on costly external financing.

The SBD is not an arbitrary subsidy, but an offsetting measure for the financing market failures that small firms face. Notably, it also partially offsets advantages enjoyed by larger firms, including access to R&D credits, accelerated depreciation, and sophisticated tax planning that smaller firms generally cannot use.

Claim: The SBD creates income-shifting opportunities

Critics also argue that a lower small‑business rate encourages high‑income individuals to incorporate and shelter personal income.

While this concern speaks more to tax design than to the existence of a lower rate, other countries address this issue differently. Estonia, for example, taxes corporate profits only when they are distributed, which supports reinvestment while largely eliminating long‑term income shifting. The lesson is clear: the problem is design, not preferential treatment itself.

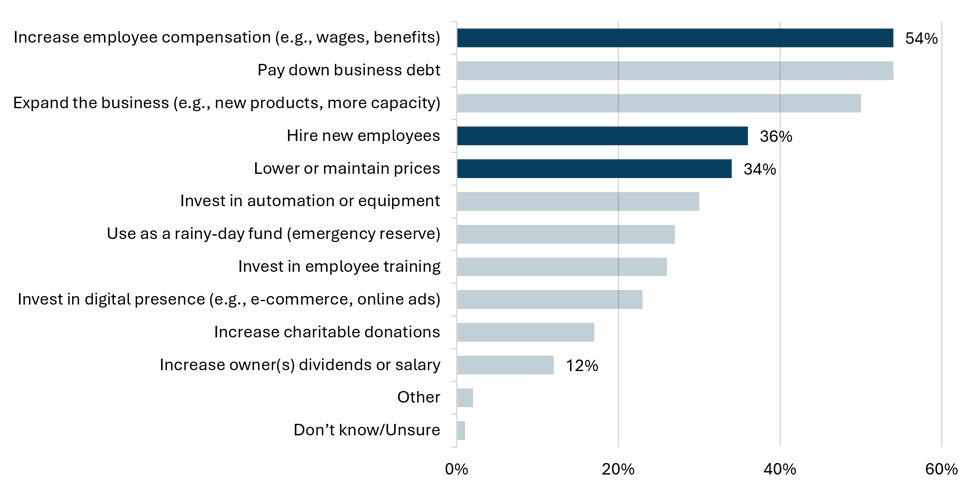

Claim: The SBD mainly benefits rich shareholders and business owners

A related criticism is that preferential small‑business tax rates mainly benefit wealthy owners, with little spillover to workers or the broader economy. CFIB survey data tell a very different story.

When asked how they would use tax relief:

- 54% of small business owners say they would increase employee compensation;

- 36% would hire new employees; and,

- 34% would lower or maintain prices.

Only 12% say tax savings would go toward higher dividends or owner compensation.

Figure 6: Small business deduction claimants, by taxable income category, Canada, 2024

Source: CFIB, Your Voice survey, July 10-24, 2025, n = 2,090.

Question: If governments at any level were to reduce the overall burden of taxes and fees, where would you allocate your savings? (Select all that apply)

These findings align with a broad body of economic research showing that corporate taxes are not paid by some abstract “corporation.” In practice, a significant share is passed on through lower wages for workers and higher prices for customers—not absorbed entirely by shareholders. The idea that raising corporate taxes is a cost‑free way to make “businesses” pay more is therefore deeply misleading.

For small firms, these effects are often magnified. They have thinner margins, less pricing power, and fewer ways to shift costs. Higher taxes show up quickly as delayed hiring, slower wage growth, or reduced resilience. Conversely, small business tax relief can translate directly into better pay, more jobs, and greater investment, especially in firms where owners and employees work side by side.

Another important takeaway from this is that the ultimate ‘cost’ to government in foregone revenue due to a lower small business tax rate is often greatly overstated, since a large share of the tax break will be recaptured downstream via income taxes, sales taxes and taxes on dividends.

Claim: A unique tax rate for all corporations would be better for the economy

Most advocates of ending the small business rate suggest that all corporations should get the same rate and that the savings from ending the small business rate be used to bring down the general corporate income rate. The logic behind this being that a tax cut for larger firms, which are taxed at the general rate, would lead to additional productivity or growth.

The problem with this approach is that it would result in higher taxes for virtually all small firms. It is difficult to argue that higher taxes on small firms will lead to additional productivity or growth. If so, we should increase taxes on everyone to encourage it.

A deeper issue: Is it time to reconsider corporate taxes?

Many debates around the SBD miss a more fundamental point: corporate taxation is an intermediate tax, one of the least efficient ways to raise public revenue. Corporate taxes are levied while income is still inside the business, before it reaches workers (salary) or business owners (dividends), raising the cost of capital and discouraging investment. Over time, much of the burden is passed on through lower wages, higher prices, or reduced business activity.

These flaws are most acutely felt by small firms. Unlike large corporations, small businesses operate with limited financial buffers and depend heavily on retained earnings to finance growth. Taxing those earnings directly erodes their capacity to invest, innovate, improve productivity, and weather economic downturns.

Put simply, corporate taxes often tax growth before it has a chance to materialize. Retained earnings are the seeds from which future productivity, wages, and tax revenues grow. Taxing them too heavily risks securing a small, immediate harvest at the expense of a larger, more sustainable one later.

Seen in this light, a 0% small‑business tax rate is not a giveaway. Because corporate taxes are an intermediate tax, eliminating them at the small‑business level does not exempt profits from taxation altogether. It simply defers taxation until profits are distributed to owners, at which point they are taxed as dividends or capital gains—as they already are anyway. This approach allows earnings to be reinvested early, when they have a high potential economic value.

Moreover, a zero rate is a pragmatic response to the high economic costs of taxing investment at the smallest scale. Manitoba’s long‑standing 0% small‑business rate demonstrates that such an approach can be targeted, administratively workable, and fiscally manageable.

None of this implies that the SBD is merely a temporary or expendable policy. Some disadvantages of operating at small scale—such as higher compliance costs, limited access to financing, and lower risk tolerance—are structural and would persist under any tax system. Other challenges stem directly from the well‑known shortcomings of taxing corporate income.

In practice, the SBD addresses both. It offsets enduring size‑based constraints while compensating for broader weaknesses in how business income is taxed. That is why strengthening the SBD in the near term and modernizing corporate taxation over the longer run are not competing agendas, but complementary ones.

Strengthening the SBD in the near term

The takeaway is clear: preferential tax treatment for small businesses is a strength, not a flaw, of Canada’s corporate tax system. At the same time, weak investment, a rapidly changing economic environment, steadily rising costs, and the current entrepreneurial drought all point to the need for a careful review of how competitive Canada’s tax system is for entrepreneurs.

CFIB has recently provided part of that review through a comparative analysis of the fiscal environment for SMEs in Canada and the U.S. It shows that Canadian microbusinesses (four employees and pre-tax net income of $150,000) pay 20% more in taxes than in the U.S., while small businesses (twenty-five employees and pre-tax net income of $1,000,000) pay 23% more.

Given today’s cost pressures and competitive challenges, the most immediate policy priority should be to strengthen the Small Business Deduction.

A few issues stand out:

-

The federal small‑business rate is now the highest in Canada. Provinces have increasingly taken the lead in supporting small businesses, leaving Ottawa behind.

The federal Parliamentary Budget Officer (PBO) estimates that each percentage point reduction of the federal small business tax rate would cost roughly $700 million, or about 0.14% of federal government revenues. CFIB is currently recommending that the rate be lowered from 9% to 6%. A reduction could also be accomplished more gradually through the introduction of more rates applying to additional corporate income thresholds. - The active income threshold is too low and not indexed to inflation. Irregular adjustments mean the real value of the SBD steadily erodes between increases, creating uncertainty and complexity.

Indexing would have broad reach at modest fiscal costs: for example, by CFIB’s calculation based on 2024 federal government data, had the limit been indexed to inflation and reached $700,000 that year, about 27,000 additional businesses would have benefited, receiving up to $12,000 each in tax relief. According to the PBO, the total cost of raising the limit to $700,000 is about $570 million, or only 0.11% of federal government revenues.

In a recent report, the Standing Committee on Industry and Technology of the House of Commons has recommended that the Government of Canada enhance the small business deduction by increasing the eligible taxable income threshold from $500,000 to $1 million. - The passive income threshold is too low and not indexed to inflation. Introduced in 2018, this rule reduces the $500,000 small business limit by $5 for every $1 of passive income (interest, rent, dividends, etc.) above $50,000. This amount has never been increased since its introduction.

Had this amount been indexed to inflation from the start, a business could now earn roughly $60,000 before reducing the small business deduction.

Allowing firms some passive investment income is a significant stabilizing source of income in tough times. Many additional firms might have failed had they not had passive investment income to help ride out the pandemic or other major shocks, which have multiplied in recent times.

CFIB is currently recommending that these challenges be recognized and the passive income amount be raised to $70,000, and indexing it moving forward. - The taxable capital phaseout range is too low and not indexed to inflation. The SBD gets phased out on a straight-line basis when a CCPC and its associated companies have between $10 million and $50 million of taxable capital employed in Canada.

Small businesses should not lose access to preferred tax treatment just because they have built up working capital to operate safely and grow. The current taxable-capital test can hit firms that keep cash or low-risk investments on hand for legitimate business reasons. The capital phaseout range should be adjusted. The lower limit of the range has been frozen at $10 million since 1994 and the upper limit has remained at $50 million since 2022. Had these amounts been indexed to inflation, the range would now be roughly $20 million - $55 million. - The delivery mechanism is overly complex. Using a deduction rather than a statutory rate has layered rules on associated corporations, passive income, and taxable capital, increasing compliance costs and confusion.

On one hand, this gives policymakers more levers to tailor the benefit, which can be scaled, phased out based on passive income or taxable capital, and adjusted without rewriting the headline rate. On the other hand, it also makes the preferential rate more intricate with rules around associated corporations, passive income grinds, taxable capital limits and debatable definitions of what constitutes a true active small business.

This design choice has also added complexity and blurred the line between core tax policy and so‑called “tax expenditures”, leading some to mislabel the SBD as a business subsidy.

Addressing these issues—by lowering the federal rate, increasing/indexing thresholds, and simplifying design—would improve competitiveness and restore the SBD’s effectiveness without introducing new distortions.

Looking ahead: modernizing how we tax business income

Over the longer term, Canada should go further and rethink its reliance on traditional corporate taxation altogether.

Many OECD countries have moved toward simpler systems, lower rates, or alternative approaches that reduce the tax burden on entrepreneurs and reinvested earnings.

In the United States, business owners can use pass‑through businesses (Sole proprietors, Partnerships, LLCs and S‑corporations), where profits are taxed on the owner’s personal tax return, not at a separate corporate level. Moreover, the Qualified Business Income Deduction, introduced in 2018 as part of the U.S. tax reform, allows owners to deduct up to 20% of their business income from their personal taxable income (for example, if you run a qualifying business and earn $100,000, you may only pay personal income tax on $80,000 of it).

Distribution‑based models, such as those used in Estonia and Latvia, tax business profits only when they are paid out. This approach avoids the double taxation of business earnings, directly encourages reinvestment and avoids many of the distortions that come with taxing retained earnings. It also offers a simpler tax structure—an important and very current consideration illustrated by the 84% of Ontario CPAs who recently said Canada’s income tax system is too complex, which led CPA Ontario to recommend that governments explore taxing distributed profits instead.

Modernization does not mean abandoning fairness or fiscal responsibility. It means recognizing that taxing intermediate production is a costly way to finance government services, especially in a small, open, investment‑constrained economy.

Conclusion and Recommendations

The evidence is clear. The Small Business Deduction remains a strength of Canada’s tax system, not a flaw. It does not meaningfully discourage growth, misallocate capital, or primarily benefit wealthy owners. Instead, it helps small firms reinvest, create jobs, and cope with the higher costs of being small.

That said, the system can and should be improved. The priority is not to abandon the small‑business tax advantage, but to restore its value, simplify its design, and ensure it continues to support entrepreneurship in a high‑cost economy.

To that end, the following policy directions deserve serious consideration:

- Strengthen the small business tax advantage by gradually lowering the small business tax rate towards 0%, a realistic objective as demonstrated by Manitoba’s 0% rate which has been in place since 2010. Focus on the federal rate first, which is now the highest among all jurisdictions in the country. Even modest reductions would provide meaningful relief and support reinvestment, jobs, and wage growth.

- Adjust and then index all SBD thresholds to inflation. This would include the active income, passive income and capital phaseout range thresholds.

- Simplify the design of the SBD. Reduce unnecessary complexity tied to associated corporations, passive income grinds, and taxable capital limits, which raise compliance costs and fuel confusion about the SBD’s purpose.

- Consider replacing the deduction with lower statutory rates or a distribution-based system. Evaluate the merits of aligning Canada with international practice by delivering the small‑business tax advantage through simpler, lower statutory rates—or by taxing profits only when they are distributed—making the system easier to understand, administer, and defend.